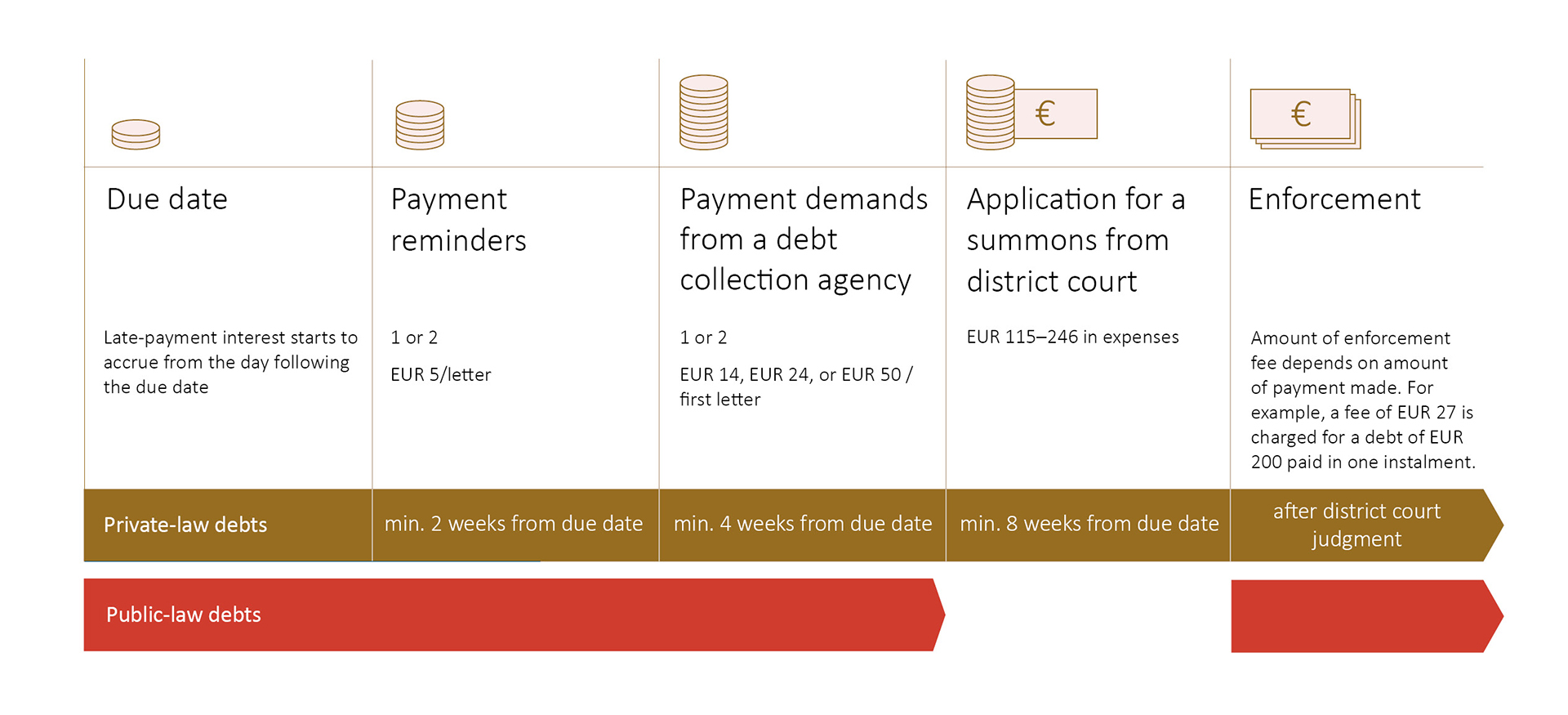

How debt collection proceeds

Collection of an unpaid bill usually proceeds in periods of two weeks. The more time has passed since the original due date, the higher the costs.

The creditor may send a payment reminder two weeks after the due date. Once two weeks have passed since the due date of the first payment reminder, the creditor may send another reminder.

If the debtor does not settle the bill after the second reminder, the creditor usually transfers it to a debt collection agency. The collection agency may send the first demand for payment four weeks after the original due date. The debt may be sent for enforcement action two months after the original due date at the earliest.

Stages of debt collection

You can download the graphic illustrating debt collection in accessible pdf format here.

Each step in the collection process generates new costs that will be added to the original bill. After the due date, the creditor may charge the contract-based interest rate in late-payment interest for 180 days. If no other interest rate has been agreed on for the debt, the interest for late payment shall be 10,5 % (reference rate fixed under the Interest Act 3,5 % + additional interest 7 %, valid from 1 January 2025 through 30 June 2025).

How late-payment interests and debt collection costs are calculated

Tips for debt collection

Even if something is difficult and complicated, you can learn to understand it if you put your mind to it. The quicker you react, the lower any unnecessary costs will be. If swept under the rug, financial matters tend to become more complicated.

Most matters can be settled, even if the situation feels insurmountable. The collection of invoices and debts causes concern, and it is common that letters are left unopened. Start settling your matters as quickly as possible.

- Open any letters sent to you and read their content. Letters give you instructions and advice on what to do in different situations. They may also forward you to advisory services.

- Sort letters based on the invoicing party and the debt number. Even if you receive a large number of letters, save them anyway. It is easier to deal with any shortcomings identified later if you have saved all your letters.

- If you feel that an invoice or debt collection process is unjustified, take action as quickly as possible by contacting the sender of the invoice. You can file a complaint regarding an unjustified invoice. (Finnish Competition and Consumer Authority)

- Negotiate a payment time extension or payment plan with a collection agency.

- If an invoice or loan is overdue, you can request voluntary collection to be suspended and the case to be transferred to enforcement proceedings. By making such a request, you can avoid any costs arising from voluntary collection and have the debt transferred for enforcement more quickly. Often, the request must be submitted in writing to the debt collection agency or invoicing party.

- The Regional State Administrative Agency supervises that debt collection agencies comply with the law and good collection practices. Read more from the Regional State Administrative Agency’s frequently asked questions.

- You have the right to obtain a statement of your debts for free once a year. The largest debt collection agencies have online services, from where you can check the amount of debts in collection free of charge using your online banking codes or another certificate.

- For advice on debt collection, contact financial and debt counselling, Takuusäätiö or the Finnish Competition and Consumer Authority’s Consumer Advisory Services.

When can a debt be transferred to enforcement?

A debt can be transferred to enforcement around two months after the original due date at the earliest. Two weeks must have elapsed since the collection agency sent its second payment demand to you.

If you wish to have your debt transferred to enforcement sooner than that, you can ask the creditor to suspend the collection measures. A prerequisite for suspending collection is that the debt has fallen due in its entirety.

Governmental and municipal charges and statutory insurance contributions

Governmental and municipal charges and statutory insurance contributions are usually directly enforceable without a district court decision. The creditor may transfer these debts to enforcement once the earlier stages of collection, such as sending payment reminders, have been completed.

Other bills

In the case of other bills than those issued by the state or a municipality, the creditor may apply for the enforcement of a debt only after a district court has issued a judgment on the debt.

The creditor or the collection agency may apply to the district court for a judgment on the debt by submitting an application for a summons to the court. The district court will forward the application for a summons to you. You should read it carefully. If you disagree with some of the information stated in the application, you can ask the Consumer Advisory Services or the financial and debt counselling services to help you with responding. You can also ask for more time to respond.

Read more

More information on the debt collection process is available on the website of the Finnish Competition and Consumer Authority.

Frequently asked questions about debt collection can be found on the website of the Regional State Administrative Agencies.